")

- Supplier Search: Apple’s reported China memory push centers on ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies (YMTC), with no confirmed deal.

- Memory Pressure: AI data centers are absorbing memory capacity, pushing Apple toward more supply options for devices.

- Policy Risk: CXMT’s Pentagon Section 1260H status creates political risk, while Entity List placement would trigger stricter licensing exposure.

- Supplier Limits: Analyst estimates and Chinese capacity limits suggest the suppliers may not quickly close Apple’s memory gap.

Apple’s reported China memory push faces U.S. scrutiny because any shift toward Chinese suppliers would sit inside a politically exposed approval path. Apple is not legally barred from buying CXMT or YMTC chips, but it faces political and reputational risk if it uses suppliers on a Pentagon blacklist.

ChangXin Memory Technologies (CXMT), a Chinese DRAM supplier, and Yangtze Memory Technologies (YMTC), a Chinese NAND flash maker, are the two names under review. Apple could evaluate CXMT DRAM and YMTC NAND flash for future devices, while any product launch remains unconfirmed.

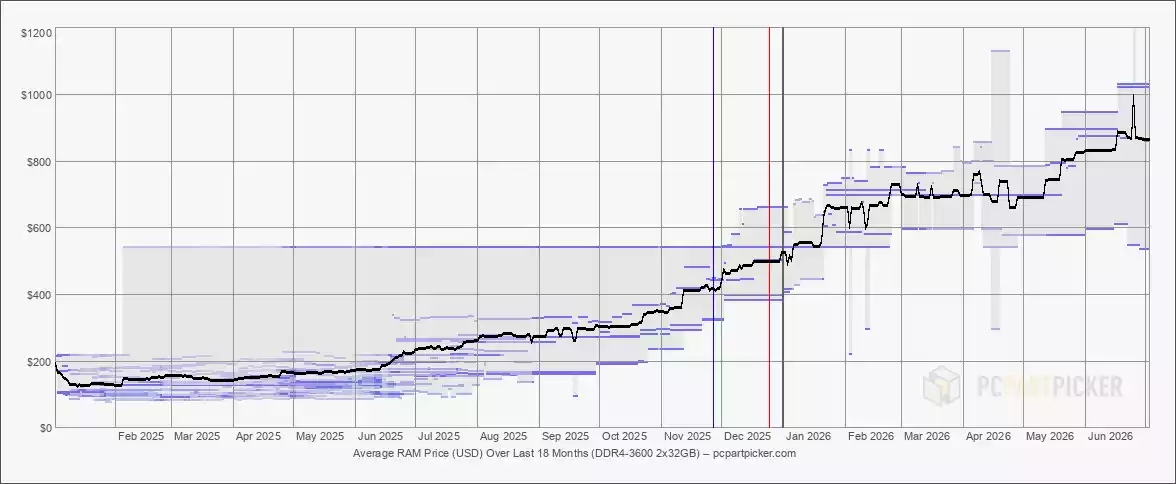

AI data centers are massively absorbing memory capacity that phone, laptop, and desktop makers also need. Market researcher TrendForce expected DRAM contract prices to rise 58% to 63% in Q2 2026. DRAM is working memory used while devices run apps; NAND flash is persistent storage that keeps data when power is off.

The increased memory pressure also reaches storage: TrendForce expected enterprise SSD prices to rise 48% to 53% over the same quarter. Any supplier contract, product launch, or regulatory approval is reported as unconfirmed in the available record.

Apple has pursued memory leverage before through Toshiba’s memory-chip sale in 2017, a distant precedent for supply-chain maneuvering rather than proof that today’s Chinese route is viable.

Supply Pressure Meets Washington Risk

U.S. scrutiny turns on a Pentagon Section 1260H list and Commerce Entity List, which create different risks: the first limits Defense Department contracting, while the second could require U.S. companies to obtain licenses before dealing with a listed company. Licensing exposure could make a supplier unusable even where a blacklist does not block a purchase outright.

The policy backdrop includes U.S. officials previously discussing potential new sanctions against CXMT as part of broader restrictions on Chinese semiconductor firms.

Analyst Ming-Chi Kuo’s warnings explain the supply side of the same problem. He ties Apple’s interest to the widening memory supply gap and warned that the memory supply-demand gap will keep widening through 2027.

Kuo estimates that 15% to 20% of consumer-electronics memory capacity in 2026 could be redirected to AI data centers in 2027. Device makers would then compete with server buyers even more for the same memory supply as they already are at the moment.

According to Kuo Apple could receive 10% to 20% fewer A20 chips than planned from the second half of 2026 through the first quarter of 2027 because of tight low-power DRAM, or LPDDR, the mobile memory format used in battery-powered devices.

Device makers face a different supply equation from cloud infrastructure buyers. AI data centers can absorb high-margin memory quickly, while consumer-electronics schedules depend on lower-power components arriving at predictable volumes. SK Hynix already overtook Samsung as memory shortages clearly extend now into 2027, reinforcing why Apple would value optionality even if the Chinese route remains politically exposed.

Why Chinese Memory Is Not a Simple Fix

The YMTC path shows why clearance is politically sensitive. Apple previously explored YMTC NAND chips for China-market iPhones in 2022 before U.S. export-control pressure and lawmaker concern halted that path.

Bipartisan Senate concern in 2022 framed YMTC procurement as a privacy, security, and global supply-chain risk. Senator Marco Rubio’s role in that earlier letter makes a similar clearance request politically sensitive in 2026.

Chinese suppliers still bring scale and pricing pressure. MS Hwang, a Counterpoint Research analyst, said Chinese memory makers matter “because they have the volume that others lack”. CXMT recorded about US$8 billion in 2025 revenue, a 130% increase from the previous year, and Chinese memory manufacturers held a price advantage of more than 15% against equivalent global specifications even as that gap narrowed.

Kuo’s capacity caveat is even sharper: limited production capacity would not materially lower Apple’s costs or fill the supply gap even if Washington allowed DRAM purchases from CXMT, and CXMT still trailed Samsung, SK hynix, and Micron by about three years in advanced DRAM node development. YMTC’s new Wuhan facility could expand storage output without solving Apple’s near-term DRAM problem. Washington’s clearance posture remains the narrow next signal for whether CXMT and YMTC become more than bargaining leverage for Apple.